Car insurance sounds simple, just a monthly payment for peace of mind if something goes wrong with your car. Yet over 215 million drivers in the US are legally required to carry some form of it, making it one of the most universal financial products out there. You might think this is just about following the law or covering accident costs, but the real story is how the type of coverage you choose can actually impact your credit, your job prospects, and your entire financial future.

Table of Contents

- What Is Car Insurance And Why Is It Essential?

- Key Types Of Car Insurance Coverage Explained

- Factors Influencing Car Insurance Rates And Choices

- Understanding Policy Terms And Coverage Limits

- Real-World Implications Of Car Insurance Decisions

Quick Summary

| Takeaway | Explanation |

|---|---|

| Car insurance is essential for financial protection | It safeguards vehicle owners against losses from accidents, theft, or damage, promoting economic stability. |

| Liability coverage is legally required | Most states mandate liability insurance, protecting drivers from financial responsibility for damages to others. |

| Consider personal risk factors when choosing coverage | Evaluate age, driving history, and vehicle type to determine the best coverage for your needs. |

| Understand key policy terms and limits | Familiarize yourself with premium, deductible, and policy limits to make informed decisions on coverage. |

| Insurance choices impact financial and legal standing | Inadequate coverage can lead to significant penalties and affect personal finances and professional opportunities. |

What is Car Insurance and Why Is It Essential?

Car insurance represents a critical financial protection mechanism designed to shield vehicle owners from potentially devastating economic consequences following accidents, theft, or damage. Unlike a simple purchase, choosing car insurance involves understanding complex risk management strategies that safeguard both personal assets and legal responsibilities.

Understanding the Fundamental Purpose of Car Insurance

At its core, car insurance functions as a contractual agreement between an individual and an insurance provider. When you select an insurance policy, you essentially transfer specific financial risks associated with vehicle ownership to the insurance company. In exchange for regular premium payments, the insurer commits to covering certain types of expenses arising from unexpected vehicular incidents.

Key Coverage Categories Include:

- Liability protection for bodily injury and property damage

- Comprehensive coverage for non collision related incidents

- Collision coverage for vehicle repair or replacement

- Uninsured motorist protection

According to National Association of Insurance Commissioners, approximately 215 million drivers in the United States carry automobile insurance, demonstrating the widespread recognition of its fundamental importance.

Financial and Legal Implications of Car Insurance

Beyond mere financial protection, car insurance serves critical legal requirements. Most states mandate minimum liability coverage, making insurance not just a wise choice but a legal necessity. Without proper insurance, drivers risk significant legal penalties, including potential license suspension, fines, and personal liability for accident-related expenses.

Choosing car insurance involves carefully evaluating personal risk factors, vehicle value, driving history, and budgetary constraints. Professional insurance agents recommend conducting comprehensive assessments that balance adequate protection with affordable premium rates. By understanding the intricate details of various policy types, drivers can make informed decisions that provide robust financial security while meeting legal obligations.

Key Types of Car Insurance Coverage Explained

Car insurance is not a one-size-fits-all solution. Different types of coverage address specific risks and provide varying levels of financial protection. Understanding these coverage types helps drivers make informed decisions when choosing car insurance that best suits their individual needs and circumstances.

Liability Coverage: Your Financial Shield

Liability coverage represents the most fundamental type of car insurance and is legally required in most states. This coverage protects drivers from financial responsibility when they cause accidents resulting in property damage or bodily injury to other parties. Typically split into two primary components:

- Bodily injury liability: Covers medical expenses, rehabilitation costs, and potential legal fees for injured parties

- Property damage liability: Pays for repairs to another person’s vehicle or property damaged in an accident

According to Insurance Information Institute, liability coverage helps protect drivers from potentially devastating out-of-pocket expenses that could otherwise lead to significant financial hardship.

Comprehensive and Collision Coverage: Protecting Your Vehicle

While liability coverage addresses damages to others, comprehensive and collision coverages protect your own vehicle. Comprehensive coverage handles damages from non-collision incidents such as theft, natural disasters, vandalism, or animal-related accidents. Collision coverage specifically addresses damages resulting from accidents involving other vehicles or stationary objects.

Drivers with newer or more expensive vehicles often find these additional coverages crucial.

To help readers compare the main types of car insurance coverage, the following table summarizes their core protection areas, what is covered, and when each typically applies.

| Coverage Type | What It Covers | When It Applies |

|---|---|---|

| Liability | Injuries to others, damage to other vehicles/property | When you are at fault in an accident |

| Comprehensive | Vehicle damage from non-collision events (theft, fire, storms) | Theft, vandalism, animal strikes, weather events |

| Collision | Damage to your car from collisions with vehicles/objects | Any at-fault or not-at-fault collision |

| Uninsured/Underinsured Motorist | Injuries/damages caused by drivers with inadequate coverage | Accident with uninsured or underinsured driver |

| Personal Injury Protection | Medical expenses for you and your passengers | Regardless of fault in an accident |

| Gap Insurance | Difference between car value and outstanding loan/lease | Vehicle is declared a total loss |

Specialized Insurance Options

Beyond standard coverages, specialized insurance options provide targeted protection for unique situations. Uninsured and underinsured motorist coverage protects you if an at-fault driver lacks sufficient insurance. Personal injury protection offers medical expense coverage regardless of accident fault, while gap insurance helps cover the difference between a vehicle’s actual value and outstanding loan balance in case of total loss.

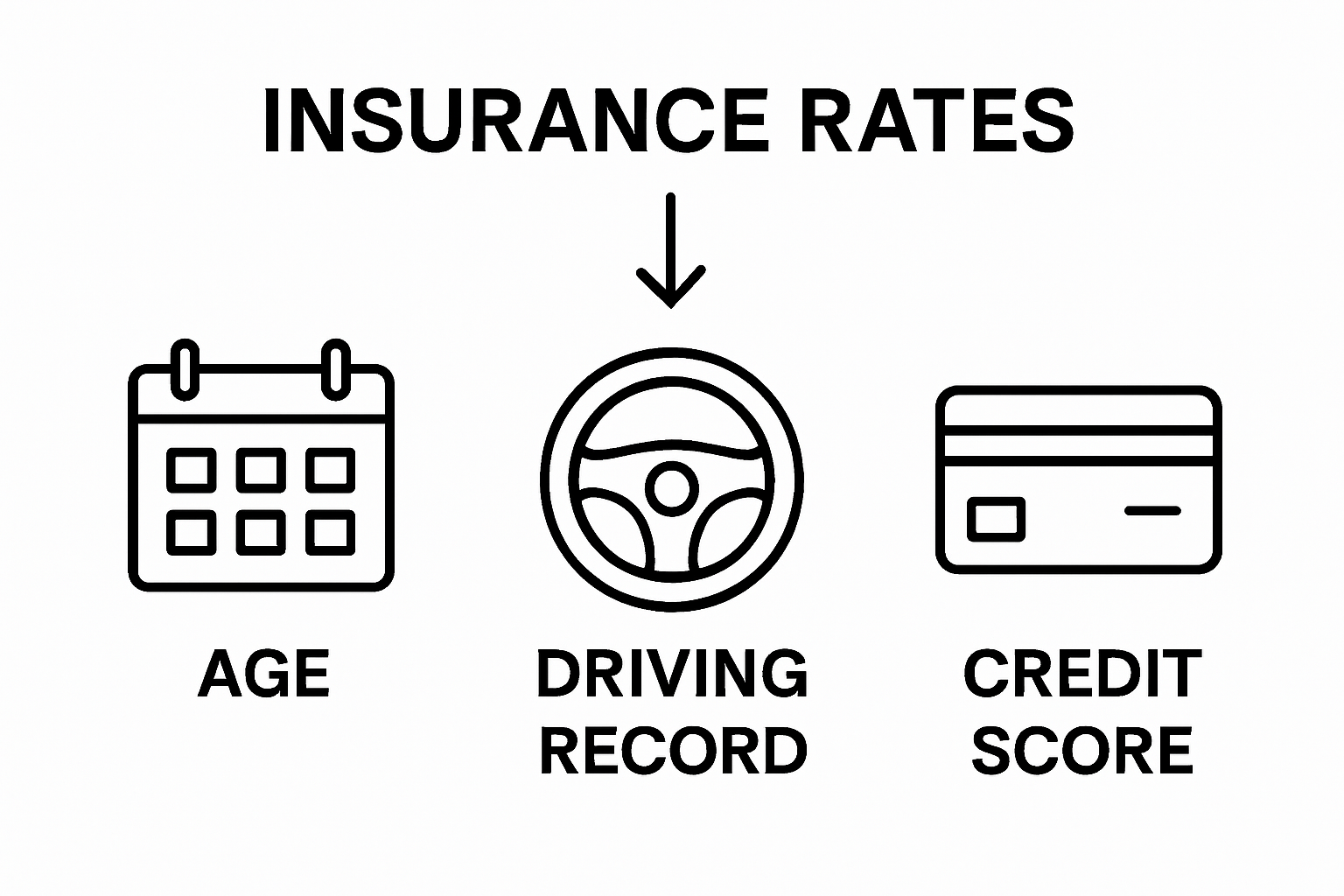

Factors Influencing Car Insurance Rates and Choices

Choosing car insurance involves navigating a complex landscape of personal characteristics, vehicular details, and risk assessment strategies. Insurance providers evaluate multiple interconnected factors to determine premium rates and coverage options, creating a nuanced pricing model that reflects individual driver profiles.

Personal Risk Profile Considerations

Drivers represent unique risk portfolios that significantly impact insurance pricing. Personal characteristics play a critical role in determining insurance rates and availability. Insurance companies analyze detailed demographic and behavioral information to assess potential financial risk.

Key Personal Factors Include:

- Age and driving experience

- Marital status

- Credit history

- Driving record and previous violations

- Occupation and annual mileage

According to the American Academy of Actuaries, these personal attributes provide insurers with comprehensive insights into an individual’s potential risk level and likelihood of filing claims.

Vehicle-Specific Insurance Determinants

The specific characteristics of a vehicle substantially influence insurance rates. Insurers meticulously evaluate vehicle attributes that could potentially increase repair costs or theft probability. Factors such as vehicle make, model, age, safety features, and historical claims data contribute to precise premium calculations.

Modern vehicles with advanced safety technologies often qualify for lower insurance rates. Conversely, high-performance sports cars or vehicles with expensive replacement parts typically incur higher premiums due to increased repair and replacement costs.

Geographic and Environmental Risk Factors

Location emerges as a crucial determinant in car insurance pricing. Urban areas with higher traffic density, increased accident rates, and greater theft risks typically experience higher insurance premiums compared to rural regions. Insurance providers analyze local crime statistics, traffic patterns, road conditions, and regional weather risks to calibrate their pricing models.

Drivers should recognize that insurance rates are not static but dynamically calculated based on an intricate combination of personal, vehicular, and environmental risk factors. Understanding these complex interactions empowers consumers to make informed choices when selecting car insurance coverage.

Understanding Policy Terms and Coverage Limits

Navigating car insurance policies requires a comprehensive understanding of complex terminology and intricate coverage mechanisms. Policyholders must decode a landscape of technical language and financial protections that directly impact their financial security and risk management strategies.

To clarify key car insurance policy terminology, this table defines essential terms that are critical for understanding your policy and coverage decisions.

| Term | Definition |

|---|---|

| Premium | The regular payment amount required to maintain your car insurance coverage |

| Deductible | The out-of-pocket amount you pay before your insurance covers a claim |

| Policy Limit | The maximum amount your insurer will pay for a specific claim or period |

| Declarations Page | A summary document listing your policy details, coverages, and limits |

| Exclusion | Specific situations or items not covered by your car insurance policy |

Deciphering Basic Policy Terminology

Every car insurance policy contains fundamental terms that define the scope and limitations of protection. Key terminology serves as the foundation for understanding insurance contracts. Drivers must familiarize themselves with critical concepts that determine their coverage and financial responsibilities.

Essential Policy Terms Include:

- Premium: Regular payment amount required to maintain insurance coverage

- Deductible: Out-of-pocket expense paid before insurance coverage activates

- Policy limit: Maximum amount an insurer will pay for a specific type of claim

- Declarations page: Document summarizing specific policy details and coverages

According to the National Association of Insurance Commissioners, understanding these fundamental terms helps consumers make informed decisions about their insurance protection.

Coverage Limits and Financial Protection Strategies

Coverage limits represent the maximum financial protection an insurance company provides for specific incident types. Drivers must strategically select limits that balance comprehensive protection with affordable premium rates. Typical coverage limits are expressed in a three-number format, such as 100/300/100, representing maximum payouts for bodily injury per person, bodily injury per accident, and property damage respectively.

Choosing appropriate coverage limits requires careful evaluation of personal assets, potential financial risks, and individual risk tolerance.

Underinsured drivers risk significant personal financial exposure, while overinsured individuals might unnecessarily inflate their premium costs.

Underinsured drivers risk significant personal financial exposure, while overinsured individuals might unnecessarily inflate their premium costs.

Navigating Policy Exclusions and Additional Protections

Insurance policies invariably include specific exclusions that define scenarios where coverage does not apply. Drivers must thoroughly review these details to understand potential gaps in their protection. Additional endorsements or riders can expand coverage beyond standard policy limitations, providing targeted protection for unique circumstances such as rental car coverage, roadside assistance, or specialized equipment protection.

Real-World Implications of Car Insurance Decisions

Car insurance decisions extend far beyond simple financial transactions, influencing personal economic stability, legal compliance, and broader societal dynamics. The choices individuals make when selecting insurance coverage can have profound and sometimes unexpected consequences that ripple through personal and professional life.

Financial Risk and Personal Economic Impact

Insurance selections directly shape an individual’s financial vulnerability. Choosing inadequate coverage can expose drivers to potentially catastrophic financial risks, while overly comprehensive policies might unnecessarily strain personal budgets. The delicate balance between protection and affordability requires nuanced decision making.

Key Financial Considerations Include:

- Potential out-of-pocket expenses during accidents

- Long-term financial protection strategies

- Impact on personal credit and financial reputation

- Relationship between insurance choices and overall risk management

- Potential savings through strategic coverage selection

According to the Brookings Institution, innovative insurance models like Pay-As-You-Drive can create substantial societal benefits by aligning insurance costs more directly with individual driving behaviors.

Legal and Professional Consequences

Insurance decisions carry significant legal implications that extend beyond simple financial protection. Insufficient coverage can result in license suspension, legal penalties, and potential professional complications. Many employment sectors require maintaining proper insurance documentation, and lapses or inadequate coverage can impact job opportunities and professional credibility.

Drivers must recognize that insurance is not merely a regulatory requirement but a critical component of responsible personal and professional risk management. The consequences of poor insurance decisions can manifest in unexpected ways, potentially limiting future opportunities and creating long-term financial challenges.

Broader Societal and Systemic Impacts

Individual insurance choices contribute to larger systemic patterns of risk distribution and economic accessibility. Insurance pricing models reflect complex algorithmic assessments of personal and collective risk, with decisions made by millions of drivers collectively shaping industry practices and social equity frameworks.

Understanding these broader implications empowers consumers to make more informed choices that not only protect personal interests but potentially contribute to more equitable and efficient insurance ecosystems.

Turn Car Insurance Protection Into Peak Vehicle Performance

Reading about car insurance choices, you know how crucial peace of mind and protection are for your vehicle and wallet. But true confidence on the road involves more than policy limits and premium payments. It calls for a vehicle you can rely on—and that means a reliable, well-tuned ECU. When your car’s performance or ECU data is at risk from an accident, technical failure, or the stresses of daily driving, the right insurance covers the cost, but restoring your vehicle to top shape requires specialized solutions.

Now you can take the next step. At ECUFlashFiles.com, you gain secure access to original and performance ECU files, fast recovery options, and expert support for every make and model. Our services go hand-in-hand with your insurance protections, helping you recover faster after an incident or simply unlock your car’s full potential. Protect what matters and keep your vehicle running smoothly—visit the ECUFlashFiles.com homepage today and discover how simple premium performance can be.

Frequently Asked Questions

What is the primary purpose of car insurance?

Car insurance primarily serves to protect vehicle owners from financial losses related to accidents, theft, or damage to their vehicle. It acts as a contractual agreement where, in exchange for regular premium payments, the insurer promises to cover certain expenses associated with unexpected vehicular incidents.

What are the main types of car insurance coverage?

The main types of car insurance coverage include liability coverage, which covers bodily injury and property damage to others; comprehensive coverage for non-collision-related incidents (like theft or natural disasters); collision coverage for automobile damage resulting from accidents; and uninsured/underinsured motorist coverage for protection against drivers without sufficient insurance.

How are car insurance rates determined?

Car insurance rates are determined by evaluating a variety of factors including personal Risk Profile (age, driving experience, marital status, driving record), vehicle characteristics (make, model, safety features), and geographic location (crime rates, traffic patterns). Insurance companies use these criteria to assess the risk associated with insuring a specific driver.

What does the term ‘deductible’ mean in car insurance policies?

In car insurance, a deductible refers to the amount a policyholder must pay out-of-pocket before the insurance coverage begins to pay for a specific claim. Choosing a higher deductible can lower premium costs, but it also means higher expenses in the event of a claim.